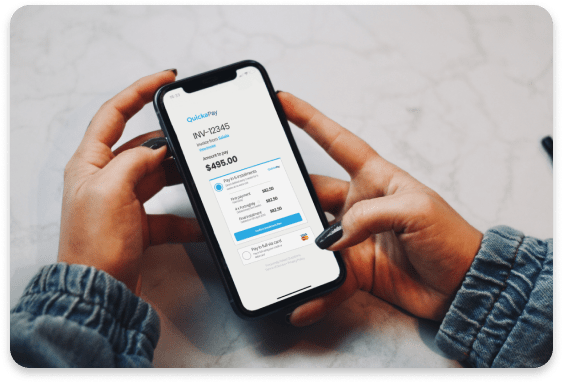

For small business owners, invoicing and payments are necessary, but time-consuming.

Getting paid on time can be challenging and put stress on cash flow.

QuickaPay helps small business owners to spend more time in the

business, and less time in the books.

It offers invoicing, card payments and BNPL with lots of easy

tech options like shareable payment links, QR codes, SMS messages and

emails. Plus it’s integrated with Shopify

and WooCommerce.

For easy reconciliations, there is a single overview of all paying

customers and exportable CSV files.

Customer refunds can also be processed directly through the

platform.https://www.quickapay.com/

Pocket money super-app Spriggy looks set for rapid expansion after banking $35m in its Series B funding round, led by NAB Ventures.The app, which helps families manage money movement by awarding pocket money and rewarding chores whilst empowering children to start managing their money responsibly with a debit card, enjoys a rapidly loyal following amongst its 500,000 family user base.This user base will likely provide the leverage for new product initiatives, as users progress on their family financial journeys into a broader range of financial tools.https://www.startupdaily.net/2021/07/fintech-spriggy-35-million-series-b-nab-ventures/

ARPA, a Beijing-based research group works on privacy-preserving computation, with a view to building the blockchain layer 2 with privacy features. The research is part of the multiparty computation (MPC) standard setting committee works with IEEE and CAICT.Could this be the future for privacy enabling blockchain use cases (fintech, property, investment, identity & access, data sharing)?https://arpachain.io/Image by Mohamed Hassan from Pixabay

Decentralized Finance is a growing global

thematic.

It promises cheaper and better access to financial services

by disintermediating centralized intermediaries.

DeFi also promises interoperability across blockchains to bust

banking silos, greatly promoting innovation and building vibrant financial

ecosystems.

However, DeFi is not without its own challenges and risks both

old and new.

The goal of automating the delivery of

financial services and reducing human dependencies also has the congruent

effect of reducing oversight and control.

This scholarly article by Nic Carter and Linda Jeng provides an excellent conceptual framework to understand

the drivers of risk in DeFi.https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3866705

Decentralised Finance (DeFi) is expected to emerge over the next decade, creating a parallel financial system operating on the internet.While bitcoin can operate as a means of payment or as a new form of commodity, DeFi projects go further, from lending to insurance and derivatives.The arrival of central bank digital currencies (CBDCs), which will enable DeFi, are perhaps five years away, while the emergence of the new internet-based finance system is probably an issue for the 2030s.Digital currencies and digital identity are an important part of enabling DeFi, and once you have these, you essentially have the missing pieces. Greg Medcrafthttp://www.afr.com/business/banking-and-finance/greg-medcraft-s-wa